David Flandro, Managing Director, Head of Industry Analysis and Strategic Advisory at reinsurance broker Howden Re, has said that “if it wasn’t obvious already, we are now firmly in the hard market softening phase of the rating cycle,” as he emphasises the need for exposure growth to be “undertaken intelligently.”

Flandro’s comments come alongside the release of Howden Re’s overview of the reinsurance industry in the first half of 2025, which highlights a clear market cycle shift amid greater competition for profitable business.

“If you look at all lines, or most lines, we are still harder in terms of pricing than we were five years ago, but it’s evident that we’ve softened recently,” said Flandro.

Building on this, Michelle To, Managing Director, Head of Business Intelligence, Howden Re, said: “Insurers are reporting decreasing rating trends due to greater competition, signalling a shift in the market cycle.”

Howden Re’s analysis is in line with CEO commentary during second quarter reporting season, with some noting that softening has occurred, but at the same time reminding that this is off of a high base after the rest in 2023, and so the business, notably property and property cat, is still attractive and profitable.

“We’re past the pricing peak. Our data show how underwriters are responding to the hard market softening phase,” added Flandro.

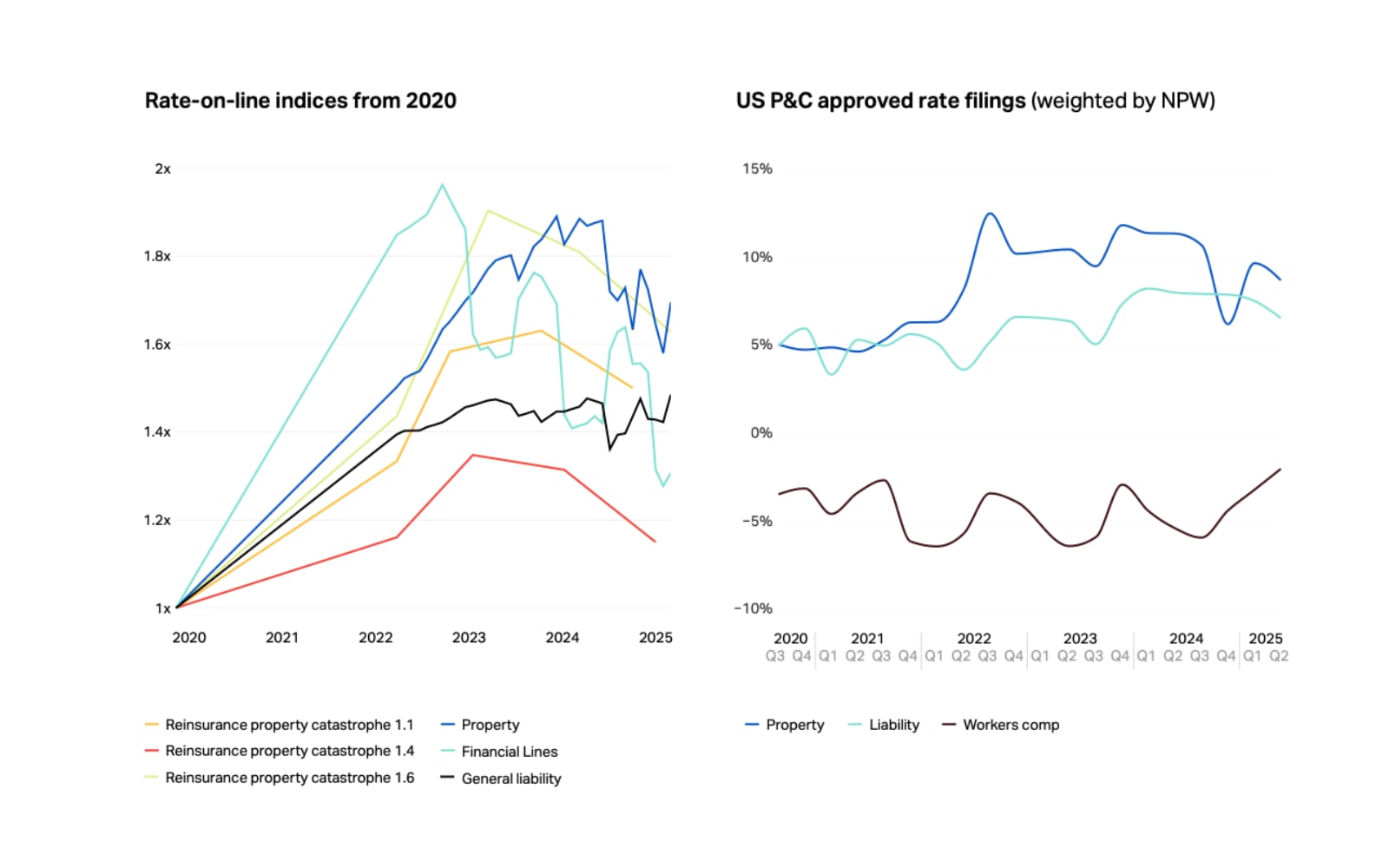

The charts below are from Howden Re’s report. The left is on a cumulative basis worldwide, and the right is the US rate filing picture.

As noted by Flandro, price changes are a different matter to premium growth, and the reinsurance broker’s report shows that, in property cat for example, while the H1’25 year-on-year rate change was -5%, premium growth for this line of business was strong at +15%. It’s a similar story for property, although less pronounced, with premium growth of +3% against a rate change of -1.4% for H1’25 when compared with the prior year.

In fact, according to Howden Re’s analysis, only liability and specialty had both positive year-on-year premium growth and rate change in H1’25, at +8% and +2% respectively, for premiums, and +1.9% and +0.4%, respectively, for rate change. For the liability reinsurance line of business, Howden Re’s data shows H1’25 year-on-year premium change of -1% and the same for rate change.

For financial lines, the broker’s data shows premium change of +4% and a rate change of -7.6% for H1’25, when compared with H1’24.

“For companies who disclose, we can see that premium is actually growing faster than pricing, and that’s an indicator that we are growing exposure in the market. This must be undertaken intelligently,” urged Flandro.

Despite the impacts of the costly Los Angeles, California wildfires in the first quarter, which according to Howden Re’s figures took natural catastrophe losses for H1’25 to a decade high of $81 billion, underwriting margins were manageable in H1’25 and solvency strong.

“Another factor affecting pricing is, of course, the reserving picture, and there’s been much discussion about this, particularly for US Commercial Auto Liability and US General Liability from accident years 2013,” said Flandro. “But to get the full picture, you need to zoom out and look at it globally on a calendar year basis. And when you do that and you include comp and short tail, you can see that reserving remains a source of profitability for most carriers in all periods from 2016. That’s significant because it bolsters carrier earnings and capital.”

The reinsurance broker’s report also highlights optimism for combined ratios going forwards, driven by manageable cat losses and diversified business models.

“Insurers are strategically adapting to the evolving market cycle through targeted growth, financial prudence and tactical portfolio rebalancing,” said To.

“Global insurance composite capital has remained steady in the first half. This has been due mainly to capital growth offset by dividends and share buybacks. Capital levels are now significantly higher than they were at the trough of 2022 due to strong profitability and asset growth. On balance, this creates more capacity, contributing to competitive pricing dynamics,” she added.

In conclusion, Flandro reiterated that it should be clear that the pricing peak is in the past. “We’re firmly in a new phase of a cycle. And in this phase, access to global top tier market data, in terms of pricing, claims, buyer behaviour and crucially profitability, by region and line of business is essential for proactive, strategic planning. The pricing tailwind has abated in order to grow top line profitably, innovation is essential.

“In summary, first half earnings and capital returns have been strong, and there’s a lot of optimism about forward earnings for 2025, and normalised combined ratios in ’26 and ’27. But again, all of this is happening in an environment of hard market softening. This is when risk selection comes to the fore.”